Letitia James, the New York State Attorney General, has presented herself as a champion of legal integrity.

Yet documents filed under oath in her late father’s estate proceedings in 1999 appear to present legal problems for James involving property law, mortgage representations, and taxation requirements.

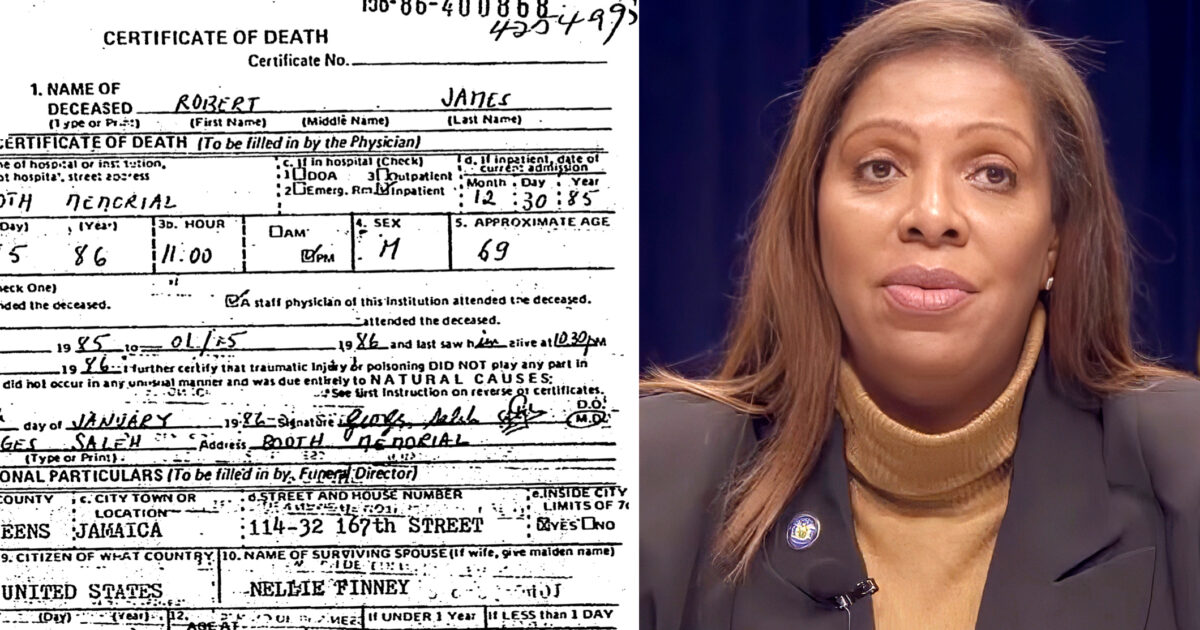

Letitia James’ father, Robert James, died on January 15, 1986. Thirteen years later, in 1999, Letitia filed a petition in Queens Surrogate’s Court seeking to administer his estate.

The only asset was a small townhome at 114-04 Inwood Street in Jamaica, Queens, a property Letitia had purchased with her father as “husband and wife” in 1983.

In sworn estate documents, Letitia claimed that the property was held as “tenants in common,” a legal classification that would require the probate court to transfer her father’s share of the house to Letitia.

“The property would not pass to the heirs of the decedent by operation of law,” James wrote in her affirmation, “because the decedent held the property with the undersigned as tenants in common with no right of survivorship.”

That distinction was crucial: unlike “joint tenancy,” which passes ownership directly to a surviving party such as a spouse, “tenancy in common” requires probate court to transfer the deceased’s share.

However, James’s account is contradicted by the mortgage Letitia and her father obtained as “husband and wife” in May 1983.

This designation implies joint tenancy with right of survivorship, meaning that ownership would have automatically passed to Letitia upon her father’s death in 1986, without the need for probate.

Then in 2000, despite her “tenants in common” probate filing in 1999, Letitia James sold the Inwood home with the original ownership listed as Robert James and Letitia James “husband and wife” anyway.

This raises the question as to whether James benefited from tax or other financial advantages by selling the property as “husband and wife,” even though she inherited her father’s interest.

Further complicating the picture is James’ 13-year delay in filing for probate. NY probate law expects reasonably prompt administration.

Though New York imposes no statute of limitations on filing probate or administration proceedings, courts expect petitions to be filed within a reasonable time, usually within a few years of death.

Letitia James’ 13-year delay is extraordinary and unexplained. A long delay implies possible concealment or misuse of the asset.

If Letitia James collected rent or claimed homeowner benefits during this period, this may amount to a breach of fiduciary duty, or at minimum, unauthorized possession of estate assets.

The publicly filed court estate documents reveal that no estate taxes – federal or state – appear to have been paid or filed in the 13 years between Letitia James’s father Robert James’ death in 1986 and her eventual filing for estate administration in 1999.

At the time of Robert James’ death in 1986, the federal estate tax exemption was $500,000. The New York State estate tax exemption was $108,333 Letitia James’s stated valuation – $105,000 in gross value, minus the mortgage – would have placed the estate below both thresholds.

However, tax attorneys caution that even non-taxable estates may be required to file estate tax returns – especially when real property is involved.

Yet, Letitia James explicitly affirmed in her 1999 petition that “There are no Federal or State Income or Estate Taxes payable by the estate.”

James also failed to indicate that a Form 706 (federal estate tax return) or a New York ET-706 (state estate tax return) had ever been filed, or that any taxes were paid in the 13-year gap between death and filing.

If estate taxes were in fact owed, this omission could constitute a violation of federal or state tax law.

Filing zero documentation over a 13-year period is highly irregular and may amount to administrative noncompliance at best – and willful evasion at worst.

By declaring no tax obligations with no supporting documentation, Letitia James effectively concealed the estate from federal and state tax authorities for over a decade.

The Robert James Estate file, which included his death certificate that appears on page 36, stands as more than a simple probate proceeding.

It serves as a documentary bridge between Letitia James’ early financial dealings and the integrity questions now surfacing amid broader mortgage fraud and campaign finance allegations.

In an era when ordinary citizens face penalties for missing tax deadlines or improperly valuing assets, the idea that the state’s top prosecutor may have dodged scrutiny for over a decade demands serious attention.

With federal investigators reportedly reviewing past mortgage filings and estate records, the 1999 estate case may prove pivotal in evaluating whether Letitia James has lived up to her own oft-quoted standard: “No one is above the law.”

Joel Gilbert, is a Los Angeles-based film producer, and president of Highway 61 Entertainment. He is on Twitter: @JoelSGilbert.

Read the entire estate document below (includes 1986 death certificate):

The post Red Flags in Letitia James Handling of Her Father’s Estate Demand Another Investigation appeared first on The Gateway Pundit.